1. Weekly News

Italy

Italy Faces Olive Oil Shortage

Italy's olive oil supply faces challenges due to rapidly reducing inventories. As of July 31, 2024, the country's total olive oil stocks amounted to 152.69 thousand metric tons (mt), marking a 14.9% month-on-month (MoM) decline from 179.42 thousand mt on June 30, 2024 and a 24.2% year-on-year (YoY) drop. In order to meet the country’s minimum olive oil reserve requirement, Italy must import over 100 thousand mt of extra virgin olive oil and around 15 thousand mt of refined olive oil by October 31, 2024,

Severe Drought Threatens Olive Groves in Italy

Olive groves in Northern Italy are experiencing unusual fruit drop in some varieties due to drought, while Sicily faces an even more dire situation with an estimated 60% drop in production compared to last year. The warm winds during the flowering period dried out the stigma, leading to flower droop and low pollination rates. In addition, high temperatures and ongoing drought have caused further damage during the fruit set phase. Despite these challenges, the oil quality remains promising, as the heat has slowed down the activity of the harmful olive fly.

Chile

Chile’s Olive Oil Exports Increased 87.6% YoY in 2024

Chile’s olive oil exports increased 87.6% YoY to USD 70 million in the first seven months of 2024. Brazil emerged as the largest export market for Chilean olive oil during this period, with an export value of USD 27 million, almost double last year. The United States (US) ranked second with an import value of USD 18 million, showing a 64% YoY increase. Spain is third, with an import value of USD 12 million, which shows a 65.6% YoY increase. In addition, Chile exported UD 23 million worth of olive oil to the European Union (EU) market. In particular, exports to Italy were USD 11 million, marking a fivefold increase YoY.

Chilean Olive Oil Industry Takes Action Against Climate Change

In Chile, the olive oil industry has strengthened its commitment to combating climate change through the Clean Production Agreement (APL), signed by the Agency for Sustainability and Climate Change (ASCC) and the Chilean Association of Olive Oil Producers (CAOOP). This new agreement aims to address environmental challenges by adopting regenerative agriculture practices and promoting the sustainable development of the olive oil sector. Key initiatives include adaptation to climate change through the efficient and sustainable use of natural resources and the circular management of waste and inputs, ensuring a more eco-conscious and resilient industry.

Spain

Reduced Olive Harvest in Extremadura, Spain

The table olive harvest in Extremadura, Spain, began on September 9, 2024, but is expected to produce smaller fruits than in previous years due to alternate bearing and drought, particularly in the Tierra de Barros region. The olive production in Manzanilla Cáceres is estimated at around 20 thousand mt. The harvest in Carrasqueña remains uncertain, largely depending on autumn rainfall. La Unión Extremadura has called for processing industries to pay a minimum of USD 1.32 per kilogram (EUR 1.20/kg) to cover production costs, threatening to report contracts below this price to the Food Information and Control Agency. Negotiations between La Unión and the industries remain stalled, creating uncertainty for the sector.

2. Weekly News

Weekly Olive Oil Pricing Important Exporters (USD/kg)

* Varieties: All pricing is for extra virgin olive oil

Yearly Change in Olive Oil Pricing Important Exporters (W36 2023 to W36 2024)

* Varieties: All pricing is for extra virgin olive oil

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

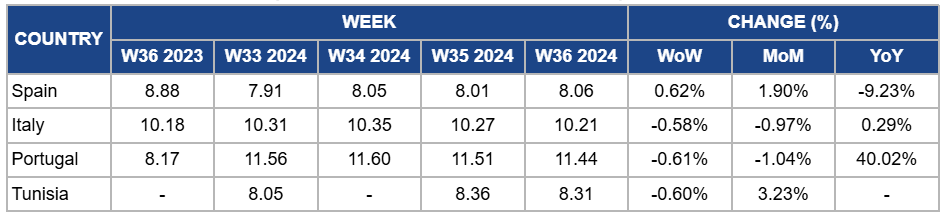

Spain

In W36, Spain's olive oil prices increased by 0.62% week-on-week (WoW) to USD 8.06/kg, reflecting a 1.90% MoM rise. However, prices decreased by 9.23% YoY, reflecting a long-term global supply recovery. The ongoing drought in the Extremadura region and lower-than-expected yields have pressured production and prices. In addition, the steady demand from export and local markets is expected to continue supporting the price before the new harvests arrive.

Italy

Italy’s olive oil prices decreased by 0.58% WoW in W36, bringing the price down to USD 10.21/kg from USD 10.27/kg in W35 due to currency change. The MoM prices fell by 0.97%, while the YoY price saw a modest increase of 0.29%. The county’s olive oil inventory dropped 14.9% MoM in Jul-24 due to steady demand. In addition, severe droughts have affected the olive groves, especially in Sicily, where production is estimated to plummet by 60% YoY. Given the current insufficient supply, the country must import significant quantities of olive oil to meet demand.

Portugal

Portugal’s olive oil prices decreased slightly by 0.61% WoW to USD 11.44/kg in W36, marking a 1.04% MoM decrease but a substantial 40.02% YoY increase. Despite the minor WoW dip, prices remain elevated due to Portugal’s role as a critical exporter to markets like Spain and Italy, which face production challenges due to extreme weather conditions. The YoY increase reflects the tight global supply and higher production costs.

Tunisia

In W36, Tunisia’s olive oil prices dropped by 0.60% WoW to USD 8.31/kg, but the MoM prices rose by 3.23%. The country’s MoM price growth reflects its ability to capitalize on the supply constraints in other major olive-producing regions like Spain and Italy. Despite climate-related challenges, Tunisia’s relatively stable production outlook allows the country to fill supply gaps in the global market, contributing to price stability despite minor weekly fluctuations.

3.Actionable Recommendations

Invest in Drought-Resistant Olive Varieties

Given the severe droughts affecting olive groves in Northern Italy and Sicily, producers should focus on investing in drought-resistant olive varieties to safeguard future yields. Research and development efforts in collaboration with agricultural institutes could accelerate the identification and adoption of these varieties. Implementing modern irrigation systems and improving water-use efficiency can help olive growers maintain productivity under increasingly challenging climate conditions.

Strengthen Position in Global Markets Amid Supply Shortages

Tunisia’s stable olive oil production outlook amid supply constraints in Spain and Italy presents an opportunity to strengthen its position in global markets. Tunisian producers should ramp up production and storage capabilities to meet rising demand. By securing long-term contracts with essential buyers in the EU, Tunisia can lock in advantageous pricing and become a reliable supplier in the face of ongoing climate challenges affecting other major producers.

Promote Climate-Smart Agricultural Practices

To build resilience against climate change, Chile’s olive oil industry should prioritize implementing regenerative agriculture practices. Producers should adopt circular management of waste and inputs, reducing environmental impact and enhancing sustainability. Workshops and training programs should be offered to farmers, helping them integrate these practices into their daily operations, thereby improving soil health and long-term production capacity.

Ensure Adequate Olive Oil Imports to Meet Reserve Requirements

Italy must prioritize securing olive oil imports to meet its reserve requirements before the end of Oct-24 before the new harvest arrives. Olive oil producers and importers should collaborate with international suppliers to establish stable supply channels from countries with available stock, such as Spain and Tunisia. Negotiating long-term contracts could also help mitigate future shortages caused by climate-induced production challenges.

Sources: Tridge, Haniotika, Oleorevista, Agromeat, OliMerca, Oleorevista