In W7 in the maize landscape, some of the most relevant trends included:

- The USDA lowered global corn reserves for 2024/25 by 1.03%, driven by weaker Chinese demand and reduced production in Argentina and Brazil.

- In Brazil, Safrinha corn planting is delayed, with only 9% of the crop planted in W7, compared to 27% in 2024. This has caused the 2024/25 corn estimate to be reduced by 2 mmt, bringing it to 123 mmt. The delayed planting raises concerns about potential yield reductions.

- Thailand’s corn imports surged by 83% YoY in the first five months of 2024/25, driven by a recovery in the pork and poultry sectors.

- US corn shipments in 2024/25 have increased 34% YoY, and US wholesale maize prices rose by 5.26% YoY to USD 0.20/kg, reflecting a reduced US corn crop estimate.

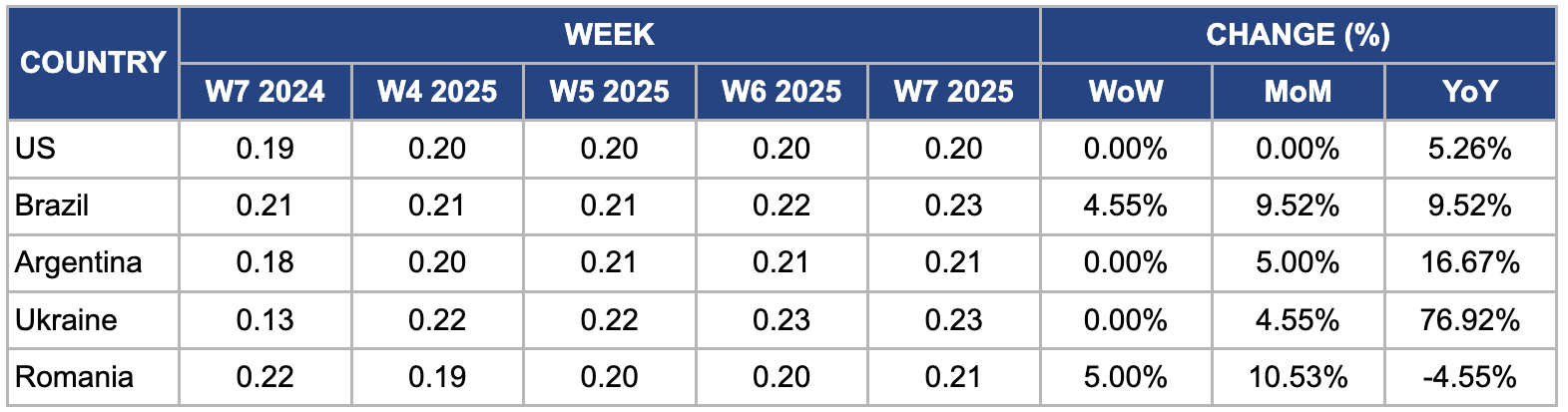

- Regarding pricing, Brazil’s maize prices rose WoW and YoY, supported by strong export demand and logistics disruptions. In Argentina, maize prices increased due to adverse weather conditions. Ukraine’s maize prices surged due to severe drought affecting production, driving up prices.

1. Weekly News

Global

USDA Lowers Global Corn Reserves Forecast for 2024/25

The United States Department of Agriculture (USDA) has lowered its global corn reserves forecast for the 2024/25 season by 1.03% to 290.31 million metric tons (mmt), primarily due to weaker Chinese demand. Moreover, corn production estimates for Argentina and Brazil have been revised downward due to declining yields. Similarly, global soybean production estimates have been cut by 4 mmt, contributing to falling corn and soybean prices. Meanwhile, Chinese imports of corn are expected to decline.

Brazil

Brazil’s Safrinha Corn Planting Lags Behind 2024’s Pace

As of late W7, Brazil's Safrinha corn planting progress was 9% complete, a significant drop compared to 27% in the same period in 2024. This marks a 6.8% weekly advance. The largest producer of Safrinha corn in Brazil, Mato Grosso, had planted 6.2% of its crop, down from 28.6% last year, as reported by the Mato Grosso Institute of Agricultural Economics (IMEA). The ideal planting window for Safrinha corn in Central Brazil is set to close around February 20, with the latest possible planting date being March 10 to 15 to avoid potential yield losses. Given the delayed planting pace, the 2024/25 Brazil corn estimate was revised downward by 2 mmt, bringing the projection to 123 mmt. The delay means that 30 to 40% or more of the Safrinha corn will be planted after the ideal window, which raises concerns about potential yield reductions. The final yield will depend on when the summer rainy season concludes, which remains uncertain.

Thailand

Thailand’s Corn Imports Surge by 83% YoY in 2024/25 MY

In the first five months of the 2024/25 marketing year (MY), Thailand’s corn imports surged 83% year-on-year (YoY), marking an 84% increase compared to the five-year average. This spike is driven by the recovery in the pork and poultry sectors, with pig production expected to reach 80% of pre-African Swine Fever (ASF) outbreak levels in 2022. According to the USDA, Thailand's corn production forecast for 2024/25 MY remains unchanged at 5.4 mmt, reflecting a 2% increase from 2023/24 MY. This growth is due to expanded planting areas and higher yields due to favorable weather and reduced drought conditions. As of Dec-24, the average farmgate price for corn stood at USD 244 per metric ton (mt), down 7% YoY. The price decline is due to higher domestic production and duty-free import influx from Myanmar and the Association of Southeast Asian Nations (ASEAN) countries.

United States

US Corn Shipments Increased by 34 Percent YoY in W6

According to USDA weekly data, for the week ending February 6, the United States (US) shipped 1.33 mmt of corn, within the expected range of 1 to 1.4 mmt. So far in the 2024/25 season, US corn shipments have totaled 23.09 mmt, showing a 34% YoY increase.

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W7 2024 to W7 2025)

United States

In W7, the US wholesale maize prices remained stable week-on-week (WoW) but rose 5.26% YoY to USD 0.20 per kilogram (kg). This increase follows the International Grains Council’s (IGC) downward revision of global corn production for 2024/25, primarily due to a lower US corn crop estimate, now projected at 377.6 mmt. This aligns with the USDA's revised forecast, reinforcing concerns over reduced supply.

Brazil

In W7, Brazil’s wholesale maize prices rose 4.55% WoW, 9.52% month-on-month (MoM), and 9.52% YoY to USD 0.22/kg. The price increase is driven by strong export demand, particularly from China, as Brazilian corn exports surged 12.3% YoY in Jan-25. Moreover, domestic logistics disruptions, including transportation delays in Mato Grosso and Paraná due to heavy rains, have slowed maize shipments to ports, tightening domestic supply. Further support comes from lower-than-expected early harvest yields in some regions, adding upward pressure on prices.

Argentina

In W7, Argentine maize prices rose by 5% MoM and 16.67% YoY, reaching USD 0.21/kg. This increase is due to adverse weather conditions, including high temperatures and insufficient rainfall, which have negatively affected maize production. As a result, the Buenos Aires Grain Exchange (BAGE) has reduced its 2024/25 production estimate by 1 mmt to 49 mmt. The primary impacts are in southern farmlands and central-eastern Entre Ríos province, where heat and dry conditions have taken a toll. If the unfavorable weather persists, further downward revisions to production and additional price increases are likely.

Ukraine

In W7, wholesale maize prices in Ukraine remained stable WoW but surged 4.55% MoM and 76.92% YoY, reaching USD 0.23/kg. This rise is due to a sharp decline in maize production driven by severe drought conditions. The USDA forecasts Ukraine’s 2024/25 MY corn output to total 25 mmt, a 23% drop from the previous season and the lowest production level since 2017. The drought has severely impacted crop yields, leading to a tighter domestic maize supply and supporting price increases.

Romania

In W7, wholesale maize prices in Romania increased 5% WoW, 10.53% MoM but declined 4.55% YoY. There is a significant reduction in maize production due to adverse weather conditions. Romania harvested only 4.88 mmt of maize from 1.8 million ha in 2024, marking the lowest since 2015. The United States Department of Agriculture (USDA) also projected Romania's maize output to drop to 7.8 mmt, the lowest level in 11 years. Moreover, many farmers have shifted from maize to more profitable crops like rapeseed, further decreasing maize cultivation areas. These factors have reduced maize supply, exerting upward pressure on prices.

3. Actionable Recommendations

Enhance Corn Storage and Export Logistics in Brazil

With rising maize prices and strong export demand, particularly from China, Brazil should prioritize expanding and modernizing its storage infrastructure. This will allow farmers to hold onto their crops during periods of price fluctuation, enabling them to sell when market conditions are more favorable. Furthermore, improving transportation networks, especially in Mato Grosso and Paraná, will help mitigate delays caused by heavy rains or other logistical disruptions. Investing in efficient road, rail, and port infrastructure is crucial to maintaining timely shipments and minimizing supply chain bottlenecks. By enhancing storage and export logistics, Brazil can strengthen its position as a reliable corn exporter, maximize profits, and ensure markets aren't excessively affected by price fluctuations.

Diversify Supply Sources in Thailand

Thailand should consider investing in technologies that increase its domestic corn production to address the surge in corn imports, particularly with rising demand from the recovering pork and poultry sectors. This could include improved seeds, more efficient irrigation systems, and crop management practices that boost resilience to adverse weather events like droughts. Moreover, expanding areas under corn cultivation can help reduce reliance on imports from countries like Myanmar and ASEAN nations. Strategic partnerships or long-term agreements with these neighboring countries could ensure a steady and predictable supply, minimizing the risk of price fluctuations driven by sudden changes in global corn availability. By diversifying sources of supply and boosting local production, Thailand can reduce vulnerability to external market shocks and secure more stable pricing for domestic industries.

Adapt to Adverse Weather in Argentina and Ukraine

In light of the severe weather conditions affecting corn production, Argentina and Ukraine should focus on improving their ability to withstand adverse weather by investing in more resilient agricultural practices. For instance, implementing advanced weather forecasting systems can allow farmers to make more informed decisions about planting and harvest times. Furthermore, adopting drought-resistant corn varieties can help mitigate the impact of inconsistent rainfall patterns and rising temperatures. Both countries should consider investing in irrigation infrastructure and soil conservation techniques that reduce the vulnerability of crops to extreme weather. By making these adjustments, Argentina and Ukraine can better protect their corn production against climate variability, ensuring more stable yields and reducing the pressure on domestic supply to help prevent price hikes during adverse conditions.

Sources: Tridge, NoticiasAgricolas, UkrAgroConsult