In W7 in the tomato landscape, some of the most relevant trends included:

- The WPTC forecasts global processed tomato production at 40.5 mmt in 2025, with China’s output expected to drop from 10.45 mmt to 6 mmt, while Spain anticipates a sharp decline from 3.1 mmt to 2.4 mmt.

- Morocco’s tomato prices fell WoW due to peak harvests, weak export demand, and logistical challenges affecting shipments to the EU and UK.

- Similarly, France’s tomato prices dropped WoW and MoM as increased domestic production and peak Moroccan and Spanish imports pressured the market.

- Türkiye’s tomato prices fell WoW as improved weather conditions boosted production in key regions like Antalya, Mersin, İzmir, and Aydın.

1. Weekly News

Global

Global Processed Tomato Output to Reach 40.5 MMT in 2025

The World Processing Tomato Council (WPTC) forecasts global processed tomato production to reach 40.5 million metric tons (mmt) in 2025, keeping it close to 2024 levels. Egypt's forecast is maintained at 780 thousand metric tons (mt), ensuring stable water availability and factory prices at USD 130/mt. Iran expects production to recover to 2 mmt after a sharp 30% decline in 2024, though currency fluctuations and geopolitical risks create uncertainty. France estimates output at 180 thousand mt, while Portugal plans to cut production to 1.4 mmt or less. Spain anticipates a significant drop from 3.1 mmt to 2.4 mmt. Canada aims to increase production slightly to 520 thousand mt, but negotiations continue. Californian farmers will reduce planted areas by 14%, which could push production to an optimistic 9.25 mmt, though actual yields remain uncertain. Chinese growers plan to cut production from 10.45 mmt to 6 mmt, reacting to weak 2024 prices. Meanwhile, Japan struggles with a shrinking planted area due to an aging farming population, prompting processors to focus on increasing harvest volumes.

Belarus

Belarus Targets 86% Tomato Self-Sufficiency by 2027 With Greenhouse Expansion

According to the Deputy Agriculture and Food Minister, Belarus aims to achieve 86% self-sufficiency in tomatoes by 2027. According to the Prime Minister, Belarus has modernized 23 hectares (ha) of greenhouse complexes, enabling full self-sufficiency in cucumbers since 2023. In 2024, domestic cucumber production exceeded demand by 161%, allowing the country to shift focus toward increasing tomato production. The government’s strategy involves 10 greenhouse projects to reduce off-season dependence on imports.

France

France Seeks EU Entry Price Reform for Moroccan Cherry Tomato Imports

The French Ministry of Agriculture has proposed modifying the European Union (EU) entry price mechanism for Moroccan tomato imports, particularly for higher-value varieties like cherry tomatoes, amid growing imports that coincide with France’s production season and spark protests from local farmers. The report highlights that the current mechanism has not evolved with import values and does not fully align with the objectives of the EU-Morocco trade agreement. Moroccan producers have shifted towards premium small-sized tomatoes, including cherry varieties, due to market demand. However, the latest regulatory changes, such as the new customs code for tomatoes under 47 millimeters (mm) effective Jan-25, fail to introduce a revised import value or entry price. As a result, Moroccan tomatoes continue to enter the EU duty-free, as their value surpasses the entry price threshold, leaving French farmers vulnerable to competitive pressure.

2. Weekly Pricing

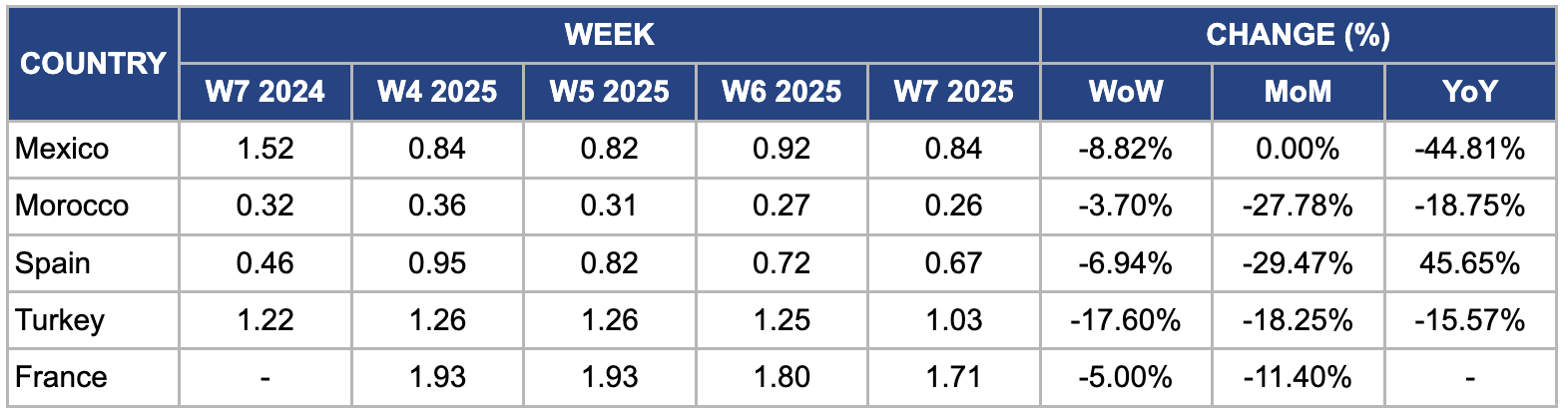

Weekly Tomato Pricing Important Exporters (USD/kg)

Yearly Change in Tomato Pricing Important Exporters (W7 2024 to W7 2025)

Mexico

In W7, Mexico's tomato prices declined 8.82% week-on-week (WoW) to USD 0.84 per kilogram (kg) from USD 0.92/kg. Year-on-year (YoY) prices dropped significantly by 44.81% compared to USD 1.52/kg in W7 2024. Merchants attribute this decline to abundant production in the Mexican Southeast. In local markets, vendors exclusively sell domestic tomatoes, with some sourcing them from Tabasco. Meanwhile, cold weather in Sinaloa, with temperatures as low as -1°C in Ahome, El Fuerte, and Guasave, resulted in 147 ha of crop losses.

Morocco

In W7, Morocco's tomato prices fell 3.70% WoW to USD 0.26/kg from USD 0.27/kg in W6, marking a 27.78% MoM decline from USD 0.36/kg in W4. This drop was primarily due to increased domestic supply due to peak harvest periods, weak export demand, and logistical challenges affecting shipments to key markets like the EU and United Kingdom (UK). Favorable weather conditions in key producing regions, including Souss-Massa and Agadir, may have boosted production, while seasonal consumption shifts likely reduced local demand. Furthermore, competition from Spain and potential trade or currency fluctuations may have weakened Morocco's export competitiveness, leading to a surplus in the domestic market and further price declines.

Spain

Spain's tomato prices fell 6.94% WoW and 29.47% MoM to USD 0.67/kg in W7. This decline is primarily due to increased domestic production and higher import volumes. Over the past decade, Spanish tomato production has decreased by nearly 19%, leading to a greater reliance on imports from countries like Morocco and Türkiye. In recent months, favorable weather conditions have resulted in abundant harvests both domestically and in these exporting countries, leading to an oversupply in the Spanish market. This surplus has exerted downward pressure on prices. Moreover, the European Union (EU) reported lower tomato prices in Feb-25 compared to previous years, with Spain experiencing prices 43% below the five-year average, further contributing to the observed price decrease.

Türkiye

In W7, Türkiye's tomato prices fell 17.60% WoW, 18.25% MoM, and 15.57% YoY, settling at USD 1.03/kg. The decline is primarily due to improved weather conditions in key tomato-producing regions, including Antalya, Mersin, İzmir, and Aydın. Benefitting from a Mediterranean climate with mild, wet winters and hot, dry summers, these areas are ideal for tomato cultivation. Earlier cold temperatures and excessive rainfall had constrained yields, but recent favorable conditions have enhanced production and supply stability. Moreover, stable export demand has helped maintain price levels without significant fluctuations.

France

In W7, France's tomato prices fell 5% WoW and 11.40% MoM to USD 1.71/kg. This was due to increased supply from domestic production and imports, mainly from Morocco and Spain, which typically peak during this period. Weaker consumer demand post-holiday season and competition from cheaper imported tomatoes may have pressured prices further. Moreover, mild winter conditions may have extended local greenhouse production, increasing availability.

3. Actionable Recommendations

Diversify Export Markets for Moroccan and Mexican Tomatoes

Moroccan and Mexican tomato producers should actively explore new export destinations beyond their traditional markets, such as the EU and the US. Expanding into Gulf countries, Southeast Asia, and Africa can help mitigate the risks associated with trade restrictions, fluctuating demand, and competition from local or regional producers. To facilitate this, exporters should work on strengthening logistics infrastructure, such as establishing direct shipping routes and cold chain storage facilities in new markets. Moreover, engaging in bilateral trade negotiations to reduce tariffs and streamline regulatory approvals can improve market access. By diversifying their export destinations, tomato producers can reduce dependency on specific regions, minimize price volatility, and ensure stable revenue streams despite changing market conditions.

Encourage CEA Investments

Mexico, Türkiye, and Morocco should prioritize investments in Controlled Environment Agriculture (CEA), including greenhouse farming, hydroponics, and vertical farming. These technologies help mitigate the impact of extreme weather events, such as frosts, droughts, and excessive rainfall, which often lead to yield fluctuations and price instability. Government and private sector initiatives can provide financial incentives, subsidies, and technical training to encourage more farmers to adopt CEA practices. Furthermore, integrating energy-efficient solutions, such as solar-powered greenhouses and precision irrigation, can enhance productivity while reducing costs. A stronger emphasis on protected cultivation will result in higher and more consistent yields, extended growing seasons, and improved quality, ensuring a more reliable supply for domestic and export markets.

Develop Value-Added Processing for Surplus Tomatoes

Mexico, Türkiye, and Morocco should focus on expanding tomato processing facilities to produce value-added products like tomato paste, sauces, purees, and dried tomatoes. This approach helps absorb excess fresh tomato supply, preventing price crashes and reducing post-harvest losses. Governments and industry players should support investments in modern processing plants with efficient production lines and cold storage capacity to improve the quality and shelf-life of processed tomato products. Moreover, producers should develop strategic partnerships with food manufacturers and retailers to secure stable contracts for their processed products. Expanding into the processed tomato market will create new revenue opportunities, stabilize farmer incomes, and reduce the industry’s reliance on fluctuating fresh tomato prices.

Sources: Tridge, Agropopular, Belta, Meganoticias, Poresto, Tomato News