In W9 in the maize landscape, some of the most relevant trends included:

- Heavy rains improved Argentina's soybean and corn outlook, but the BCR lowered its corn forecast to 46 mmt, while the USDA maintained 50 mmt.

- Safrinha corn planting reached 36% in Brazil, lagging behind last year’s 59%, though drier W9 weather may accelerate progress. CONAB still projects 122 mmt corn production.

- Regarding pricing, US prices fell WoW due to strong early sales to Mexico. Brazilian prices rose WoW due to strong Chinese demand and logistics disruptions. Ukraine’s prices surged YoY due to severe drought-cutting supply.

1. Weekly News

Argentina

Heavy Rains in Argentina Improved Corn Prospects After Dry Spell

Heavy rains across Argentina’s key agricultural regions are expected to persist for several more days, improving the outlook for soybean and corn harvests, according to the Rosario Grain Exchange (BCR). Over 100 millimeters (mm) of rainfall in recent days has helped crops recover from drought and the extreme heat experienced on Jan-25 and Feb-25. As a top global grain exporter, Argentina relies heavily on wheat, corn, and soybean product exports for foreign exchange earnings. Previously, dry conditions prompted the exchange to lower its 2024/25 and corn to 46 million metric tons (mmt), while the United States Department of Agriculture (USDA) maintains higher estimates of 50 mmt.

Brazil

Mato Grosso Leads Brazil’s Safrinha Corn Planting Progress

As of late W8, Brazil's Safrinha corn planting reached 36%, significantly behind 59% in 2024 but advancing 16% weekly, with Mato Grosso leading at 45% planted. A drier forecast in W9 should accelerate soybean harvesting and Safrinha corn planting, easing concerns over delayed sowing beyond the ideal window, particularly in Paraná and Mato Grosso do Sul. Meanwhile, first-crop corn harvesting progressed to 29%, compared to 34% last year, with an 11% weekly advance. The National Supply Company (CONAB) maintains its initial estimate for Brazil's 2024/25 total corn production at 122 mmt despite planting delays raising concerns over potential yield risks in later-planted areas. Moreover, Safrinha cotton planting in Mato Grosso is nearly complete at 95.6%, slightly above the 94.9% historical average. Farmers are expected to make further planting progress this week, likely surpassing the average pace, with late planting risks now lower than initially feared.

Saudi Arabia

Saudi Arabia’s Corn Demand to Grow 5% Annually Amid Declining Local Production

Saudi Arabia, a key grain market in the Middle East, is expected to see steady domestic demand growth in 2025, with corn consumption projected to increase by 5% year-on-year (YoY). The country currently imports 5 mmt of corn, primarily from Argentina, Brazil, and Ukraine, while domestic production remains minimal at 100 thousand metric tons (mt) to 150 thousand mt, reinforcing its reliance on imports.

United States

US-Mexico Corn Trade Faces Uncertainty Amid Potential Trade War

The United States (US) is on the brink of a potential trade war with Mexico, its largest corn buyer, raising concerns over future purchasing trends. Despite concerns over potential import reductions, current data shows no immediate trade disruptions. As of mid-Feb-25, Mexico had secured a record 17.2 mmt of US corn for shipment in the 2024/25 season, accounting for 70% of the USDA’s projected Mexican corn imports. This suggests that Mexican buyers may have accelerated purchases in anticipation of trade tensions, but whether future imports will decline remains uncertain.

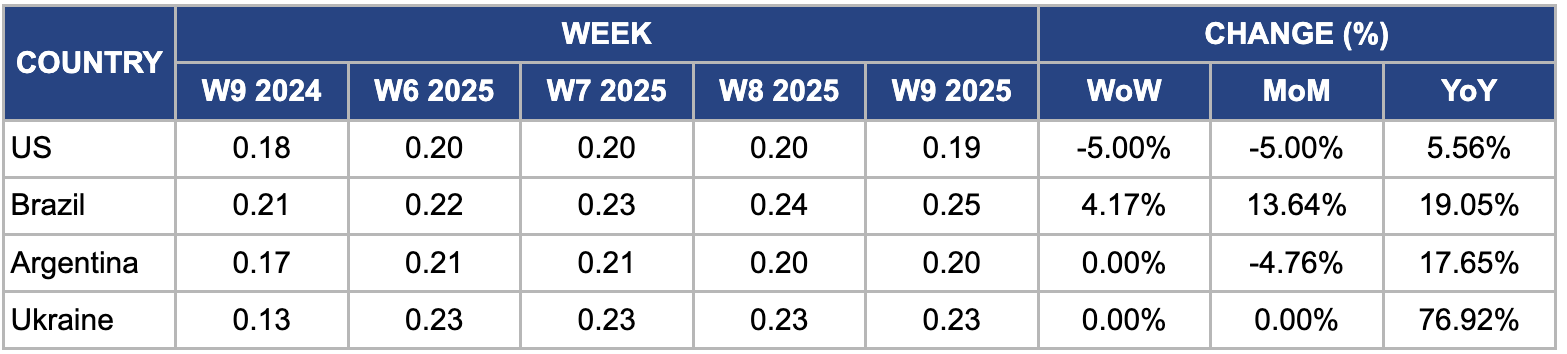

2. Weekly Pricing

Weekly Maize Pricing Important Exporters (USD/kg)

Yearly Change in Maize Pricing Important Exporters (W9 2024 to W9 2025)

United States

In W9, the US wholesale maize prices declined 5% week-on-week (WoW) and month-on-month (MoM) to USD 0.19 per kilogram (kg). This was primarily driven by improved weather conditions aiding harvest progress and increased farmer sales. Moreover, the US had already sold 17.2 mmt of corn to Mexico as of late W8, fulfilling 70% of the USDA’s forecast for Mexico’s total corn imports in the 2024/25 marketing year (MY). This early sales surge reduced immediate demand pressure, contributing to the price decline.

Brazil

In W9, Brazil’s wholesale maize prices rose 4.17% WoW, 13.64% MoM, and 19.05% YoY to USD 0.25/kg, driven by strong export demand, particularly from China, as Brazilian corn exports surged 12.3% YoY in Jan-25. Domestic logistics disruptions, including transportation delays in Mato Grosso and Paraná due to heavy rains, have slowed maize shipments to ports, tightening domestic supply. Moreover, lower-than-expected early harvest yields in some regions have further pressured prices upward.

Argentina

In W9, Argentine maize prices remained unchanged WoW but declined 4.76% MoM to USD 0.20/kg due to improved supply conditions as the harvest progressed, increasing market availability. Favorable weather in key maize-producing regions, such as Buenos Aires, Córdoba, and Santa Fe, likely supported higher yields, contributing to the price drop. Currency fluctuations and macroeconomic instability influenced price movements. The Argentine peso’s depreciation against the US dollar boosted export competitiveness, leading to higher shipments and potentially increasing domestic supply. However, inflation and financial instability may have impacted production costs and farmer selling decisions, adding to price volatility.

Ukraine

In W9, Ukraine’s wholesale maize prices remained stable WoW but surged 76.92% YoY to USD 0.23/kg, driven by supply concerns amid a sharp decline in domestic production. Severe drought conditions throughout the growing season significantly reduced yields, limiting overall supply. The USDA projects Ukraine’s 2024/25 MY corn output at 25 mmt, marking a 23% YoY decline and the lowest production level since 2017. The drought stunted crop development and delayed harvest progress in some regions, exacerbating supply constraints. With tighter domestic availability and strong global demand, particularly from key export markets, maize prices continue to receive upward support.

3. Actionable Recommendations

Leverage Argentina’s Favorable Weather for Export Expansion

With recent heavy rains improving maize yield prospects, Argentine exporters should accelerate forward contracts and lock in sales at current global prices before a potential increase in supply pressures prices downward. Targeting Saudi Arabia, which is set to increase corn imports by 5% YoY, and Mexico, where trade tensions with the US might lead to demand diversification, could be key opportunities. Securing contracts early mitigates price volatility risks while ensuring a steady revenue stream. Moreover, leveraging a depreciating peso makes Argentine maize more competitive.

Optimize Brazil’s Logistics to Avoid Domestic Supply Tightness

Brazil's heavy rains have caused transportation delays, tightening domestic supply and increasing maize prices. Investing in improved logistics planning, such as rail and port infrastructure efficiency, can ease bottlenecks and ensure steady shipments. Encouraging private sector partnerships in grain transportation networks can help mitigate future disruptions. A smoother export flow will reduce domestic price spikes while ensuring Brazilian maize remains attractive to buyers like China. Strengthening logistics also enhances long-term export reliability.

Diversify Ukraine’s Maize Market to Offset Supply Constraints

Given Ukraine’s 76.92% YoY price surge due to production declines, exporters should diversify beyond traditional European buyers and target higher-value markets in Asia and the Middle East. Promoting long-term contracts with Saudi Arabia and China and investing in alternative shipping routes to bypass Black Sea disruptions can ensure stable sales. Expanding market reach will help mitigate revenue losses from lower production while securing long-term buyers amid supply concerns.

Sources: Tridge, Graintrade, Hellenic Shipping News, UkrAgroConsult