W20 2025: Beef Weekly Update

.jpg)

In W20 in the beef landscape, some of the most relevant trends included:

- Global cattle prices are expected to rise through 2025 due to tightening supply and growing demand, amid an expected 3% YoY drop in beef production from key exporters and shifting trade markets.

- Mexico’s cattle exports dropped 52% YoY in Q1-2025 due to US border closures caused by screwworm outbreaks.

- The UK’s NFU welcomed beef access and food standards in the US-UK deal but worried bioethanol tariff cuts may hurt local producers.

- US beef imports under low-tariff quotas rose 14% YoY, led by Australia and New Zealand, while some US states ban or regulate lab-grown meat to protect traditional livestock.

- The US meat industry faces tariff challenges in Vietnam’s growing market as it competes with CPTPP members benefiting from zero tariffs.

1. Weekly News

Global

Cattle Prices Expected to Rise in 2025 as Supply Tightens and Global Demand Surges

Global demand for cattle and beef is rising steadily across Africa, Asia, and Latin America, fueled by strong market interest amid declining production in key regions such as Brazil, New Zealand, and Europe. This growing imbalance between supply and demand is expected to drive cattle prices higher through the end of 2025. According to the World Agricultural Supply and Demand Estimates (WASDE) and RaboResearch, global beef production is projected to decline by 3% year-on-year (YoY) in 2025, largely due to reduced output in Brazil and New Zealand.

Similarly, red meat production in European countries like Germany, France, and the Netherlands is either stagnant or declining, as reported by the Agriculture and Horticulture Development Board (AHDB). In the United States (US), red meat exports may be impacted by Chinese retaliatory tariffs in May-25, prompting US exporters to diversify into alternative markets such as Japan, Mexico, South Korea, Central America, and Taiwan. However, a 90-day tariff rollback agreement featuring a 115% downward adjustment between the US and China, effective from May 14, could offer temporary relief and help stabilize bilateral trade. Meanwhile, the European Union (EU) has increased its red meat shipments to emerging markets like Algeria and Turkey.

Mexico

Mexico’s Cattle Exports Drop 52.3% YoY in Q1-2025 Following US Border Closures Due to Screwwarm Outbreaks

Mexico’s cattle exports plunged 52.3% in Q1-2025 to USD 163 million from USD 341 million in Q1-2024, mainly due to US border closures caused by screwworm outbreaks. After the New World Screwworm (NWS) was detected in southern Mexico in Nov-24, the United States Department of Agriculture (USDA) halted live cattle trade, leading to a historic zero beef export value in Jan-25, the first since 1993. Exports resumed in Feb-25 following a joint inspection and treatment protocol by the Animal and Plant Health Inspection Service (APHIS) and the Service for the National Health for Food Safety and Food Quality (SENASICA). A new closure starting May 11, expected to last until May 25, could cost the livestock sector USD 11.4 million daily, heavily impacting northern states Sonora and Chihuahua, which export over 5,700 cattle daily at around USD 2,000 each. Working with US authorities, Mexico’s Ministry of Agriculture is intensifying surveillance, controlling animal movements, and releasing sterile flies to combat the outbreak and reopen the border.

United Kingdom

UK-US Trade Deal Sparks Praise and Concern

The United Kingdom’s (UK) National Farmers Union (NFU) offered a mixed reaction to the recently signed US-UK economic agreement. While the union welcomed the preservation of UK food standards and the establishment of reciprocal market access for beef, it raised concerns over the removal of tariffs on US bioethanol. Under the agreement, both countries are granted a beef quota of 13 thousand metric tons (mt), a move the NFU viewed as a positive step toward fair trade that safeguards the UK’s domestic food standards, particularly the continued prohibition of US beef produced with growth hormones. The US Agriculture Secretary described the deal as a major opportunity to expand US beef exports to the UK. However, analysts highlighted that comparable pricing and strong consumer preference for British and Irish beef, especially among leading retailers such as Tesco and Sainsbury’s, could limit market penetration for US products. Meanwhile, the NFU expressed concern that full US access to the UK bioethanol market may adversely affect domestic producers, arguing that agriculture is being disproportionately burdened by trade-offs made to support other economic sectors.

United States

US Beef Imports Under Low-Tariff Quotas Rise 14% YoY as Supplier Trends Shift

As of May 5, US beef imports under low-tariff quotas totaled 288 thousand mt, reflecting a 14% YoY increase. Performance among suppliers varied, with Australia registering a 29% YoY increase in shipments, while New Zealand and Argentina growing theirs by 12% to 13% YoY. However, Uruguay saw a 35% YoY decline. Despite these disparities, all four major quota-holding countries—Australia (378 thousand mt), New Zealand (213 thousand mt), and Argentina and Uruguay (20 thousand mt each)—had utilized between 34% and 37% of their annual allowances. On the contrary, a 65 thousand mt third-country quota, primarily used by Brazil and slightly by Paraguay, was fully exhausted within 15 days of 2025, leading the US to reallocate 13 thousand mt to the UK. Meanwhile, Canada and Mexico continue to export beef to the US duty-free and without limits under the United States-Mexico-Canada Agreement (USMCA).

US Meat Industry Faces Tariff Hurdles in Vietnam's Growing Import Market

The US meat industry is working to solidify its position in Vietnam, where rising urbanization, increasing incomes, and a growing middle class are fueling demand for imported meat. However, US exporters face stiff competition due to high Most Favored Nation (MFN) tariffs, 10% on frozen pork and up to 30% on beef, while the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) member countries such as Canada, Mexico, Australia, and New Zealand benefit from zero tariffs under free trade agreements. Despite this, US industry groups are emphasizing the high quality and safety of American meat while partnering with local importers. Trade tensions escalated in Apr-25 following a proposed 46% US tariff on Vietnamese goods, later temporarily reduced to 10% under a 90-day suspension. Despite Vietnam’s offer to lower tariffs on US imports and curb Chinese transshipment practices, supply chain disruptions persist. To remain competitive, US meat exporters are pushing for improved trade terms and exploring future free trade agreements with Vietnam.

Indiana, Montana, and Oklahoma Target Lab-Grown Meat with Bans and Labeling Rules

Several US states are cracking down on lab-grown and imitation meat to protect traditional livestock industries. Indiana will enforce a two-year ban on cultured meat sales starting July 1, requiring clear labeling as “This is a meat imitating product.” Montana’s House Bill 401 bans the manufacture and sale of cell-cultured meat from October 1, 2025, with violations resulting in fines or jail time. Oklahoma’s House Bill 1126, effective November 1, 2025, mandates that plant, insect, and lab-based protein products be clearly labeled and not falsely advertised as meat. Meanwhile, the National Cattlemen’s Beef Association (NCBA) is urging the Food and Drug Administration (FDA) to strengthen federal labeling rules to prevent imitation meat producers from using terms and imagery associated with real beef.

2. Weekly Pricing

Weekly Beef Pricing Important Exporters (USD/kg)

* Varieties: Brazil (boneless rear beef), Australia (young cattle indicator), US (lean 92-94%), India and Argentina (overall beef)

Yearly Change in Beef Pricing Important Exporters (W20 2024 to W20 2025)

* Varieties: Brazil (boneless rear beef), Australia (young cattle indicator), US (lean 92-94%), India and Argentina (overall beef)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

Brazil

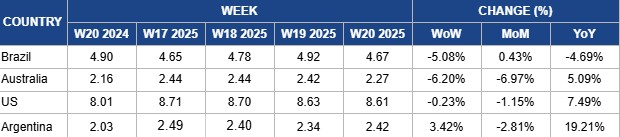

In W20, Brazil’s wholesale boneless rear beef prices fell by 5.08% week-on-week (WoW) to USD 4.67/kg, down 4.69% YoY but still 0.43% higher month-on-month (MoM). The decline is largely attributed to an increased supply of slaughter-ready cattle and buyers’ reduced willingness to pay higher prices. As the rainy season ends, pasture conditions are deteriorating, prompting ranchers to accelerate sales. This has weakened sellers' bargaining power in a market with subdued consumption. Safras and Mercado expect continued downward pressure on prices in the short term, especially due to the abundant cattle supply in the Center-North region.

Australia

Australia’s National Young Cattle Indicator averaged USD 2.27/kg in W20, down 6.20% WoW and 6.97% MoM, though still 5.09% higher YoY. According to Meat and Livestock Australia (MLA), the cattle market softened overall, with the restocker yearling steer indicator remaining steady. After last week’s record yardings, numbers fell by 25 thousand heads to 76.45 thousand heads. Prices at key saleyards like Wagga Wagga dropped by 33% WoW, with Roma showing a similar trend, likely due to reduced saleyard throughput as yardings decreased by 765 heads. The feeder market weakened across all states except Queensland, where prices held firm. Lightweight steer prices eased, while medium weights gained support amid limited heifer availability.

United States

In W20, US lean beef (92% to 94% lean) averaged USD 8.61/kg, marking a slight 0.23% WoW decline and a 1.15% MoM drop, likely due to softened demand after recent record highs. Despite five consecutive weeks of easing, prices have remained above USD 8.60/kg, indicating underlying market resilience. With the recently implemented import tariffs impacting consumer budgets, food companies are leveraging promotions to attract price-sensitive buyers. Despite the recent price drops, quotations are still 7.49% higher YoY, supported by tightening domestic supply linked to a shrinking national cattle herd. According to the USDA, the total US cattle herd stood at approximately 86.7 million heads as of January 1, down from 87.2 million in Jan-24, with beef cow numbers falling 1% YoY to 28 million heads, the lowest inventory since 1951. Supply pressures are expected to intensify following the suspension of live cattle imports from Mexico on May 11 due to the NWS outbreak. This disruption is expected to further tighten US beef supply, likely pushing prices upward in the coming weeks, especially with the summer grilling season approaching.

Argentina

Argentina’s average steer beef price rose to USD 2.42/kg in W20, marking a 3.42% WoW increase and a significant 19.21% YoY surge. However, the price remains 2.81% lower MoM. Interestingly, in the local currency, the prices averaged ARS 2,735.98/kg (USD 2.42/kg) in W20, a 2.92% drop from ARS 2,818.41/kg (USD 2.34/kg) registered in W19. This indicates that the WoW rise in USD was influenced by currency fluctuation. Nevertheless, the significant YoY rise reflects broader challenges, including reduced beef consumption in 2024 amid ongoing economic difficulties. Besides that, supply-side concerns are mounting as the USDA projects Argentina’s beef production to drop by 3% YoY to 3.08 million metric tons (mmt) in 2025. This is underpinned on a revised cattle slaughter estimate of 13.4 million heads due to early sell-offs driven by drought and high production costs. The national herd has decreased to 52.37 million heads, the lowest in years, due to poor calving rates and adverse weather conditions. Domestic beef consumption is expected to hold steady at 2.31 mmt in 2025, similar to 2024 levels, though economic constraints continue to reduce per capita intake. This situation has boosted the preference for pork and poultry. A recovery in consumer spending could potentially revive domestic beef prices.

3. Actionable Recommendations

Optimize Low-Tariff Quota Use and Explore Flexible Reallocation Mechanisms in the US

As US beef imports under low-tariff quotas continue to rise amid changing supplier dynamics, the US should optimize quota allocation efficiency and explore flexible reallocation mechanisms. The swift exhaustion of Brazil’s third-country quota by mid-Jan-25 signals strong demand and highlights the need to redesign quota distribution policies. The US government should consider introducing real-time tracking and dynamic reallocation systems that respond to supplier fill rates, allowing underutilized quotas like in the case of Uruguay to be reassigned more efficiently to high-demand countries. Meanwhile, fostering long-term trade relationships with Australia, New Zealand, and Argentina should include capacity-building in compliance and cold chain logistics to ensure quality consistency across suppliers.

Negotiate Preferential Access and Highlight Quality to Compete in Vietnam’s Meat Market

Facing high MFN tariffs in Vietnam and growing competition from CPTPP countries, US meat exporters should strengthen lobbying efforts for preferential trade terms and focus on value-based marketing. Industry associations should actively engage with US trade officials to push for bilateral or multilateral negotiations that replicate CPTPP-like benefits, particularly lower tariffs on beef and pork. Simultaneously, exporters should invest in awareness campaigns that promote the safety, traceability, and superior flavor of US meat. Working with local distributors to develop co-branded products and localize packaging and labeling could improve market appeal. Until trade terms improve, focusing on high-end foodservice channels and premium retail outlets offers a viable interim strategy.

Accelerate Disease Control and Cross-Border Collaboration to Restore Mexico’s Cattle Export Capacity

The screwworm outbreak in Mexico, which caused a drastic 52.3% YoY decline in cattle exports in early 2025, highlights the urgent need for coordinated disease control efforts and stringent border protocols. Authorities should prioritize accelerating joint inspections, surveillance, and innovative control measures such as sterile insect releases to contain outbreaks quickly and reopen US borders. Investment in biosecurity infrastructure and regional collaboration between Mexico and the US will be vital to safeguard livestock health, restore trade flows, and minimize economic losses, estimated at USD 11.4 million daily during border closures.

Sources: Tridge, Agromeat, Agravery, UkrAgroConsult