W33 2025: Beef Weekly Update

.jpg)

In W33 in the beef landscape, some of the most relevant trends included:

- Argentina’s beef consumption is rising, averaging 50.24 kg per capita in Jul-25. However, producers face pressure from Brazilian imports, export duties, and Chile’s suspension of Patagonia shipments over FMD concerns.

- Brazil is expanding its global reach, pursuing new market openings in Central America, the Caribbean, and Asia, while edging closer to access to Japan’s premium beef market.

- China’s beef production reached 3.42 mmt in H1-2025, driven by demand and culling, while Jun-25 saw imports rebound, boosting prospects for Brazilian exporters.

- Paraguay stands to benefit from US tariffs on Brazilian beef, positioning its exports as more competitive despite higher costs, with shipments and revenues already surging.

- South Korea’s strong loyalty to Hanwoo beef, supported by the Korean Beef Act and origin-focused preferences, sustains the sector despite cost pressures and import competition.

1. Weekly News

Argentina

Beef Demand Increases in Argentina as Imports Challenge Local Producers

According to the Ministry of Agriculture, Argentina’s beef sector is experiencing a surge in domestic consumption, with per capita intake rising to 50.24 kilograms (kg) in Jul-25, driven by improved purchasing power and strong cultural preference for meat. According to the Beef Promotion Institute (IPCVA), beef prices climbed 58% in the past year, boosting cattle values across categories. However, rising imports from Brazil have introduced new competition, with 8 thousand metric tons (mt) of beef already entering the country in 2025. While these imports remain relatively small in volume, they represent a disproportionate outflow of foreign currency, undermining local producers who also face export duties. The situation is further complicated by Chile’s recent suspension of Argentine beef imports from Patagonia due to health concerns over foot-and-mouth disease (FMD). This highlights how domestic policies are creating both trade imbalances and sanitary risks. These factors show that despite robust domestic demand, Argentina’s beef industry is under pressure from policy decisions, import dynamics, and external trade restrictions.

Brazil

Brazilian Agribusiness Strengthens Global Reach with New Market Openings

On August 8, Brazil’s Ministry of Agriculture, Livestock and Food Supply (MAPA) launched a mission to Central America and the Caribbean to strengthen agricultural trade and cooperation, beginning in Panama with discussions on animal protein, fruits, and health agreements. The mission continued on August 11 in Barbados, where negotiations focused on opening the market for Brazilian beef, poultry, and grain exports. At the same time, the Arab-Brazilian Chamber of Commerce urged redirecting products hit by United States (US) tariffs, such as beef, coffee, and sugar, toward Arab markets such as Saudi Arabia, Egypt, and the United Arab Emirates (UAE).

Brazil has also finalized health protocols with the Philippines for bone-in beef and offal, adding to more than 400 market openings since 2023. Meanwhile, Brazil is close to securing long-awaited access to Japan’s beef market, with southern states poised to lead exports due to their FMD-free status. This opens opportunities in one of the world’s most demanding and high-value markets.

China

China’s Beef Market Strengthens with Rising Production and Renewed Import Demand

In the first half of 2025 (H1-2025), China’s beef sector showed resilience, with production reaching 3.42 million metric tons (mmt) and prices recovering despite broader oversupply challenges in other meats. The rise in beef output was largely linked to the slowdown in the dairy sector and the culling of breeding stock, which boosted slaughter volumes, while stable supply and firm domestic demand supported price stability. Unlike poultry, which faces oversupply and falling prices, beef imports rose in Jun-25 for the first time in 2025, easing pressure on foreign purchases and signaling renewed demand for overseas suppliers. This creates a favorable outlook for Brazil, as China’s ongoing safeguard investigation into beef could lead to lower tariffs or a high, non-exclusive quota. This situation could enhance Brazilian competitiveness and raise expectations for stronger beef exports to the world’s largest meat market in the second half of the year.

Paraguay

Paraguay Gains Edge as New US Tariffs Weigh Heavily on Brazil’s Beef

Effective from August 7, the new US tariffs will impose a 15% minimum rate on countries with a negative trade balance and 10% on those with a positive balance, including Paraguay. While this represents an additional cost for Paraguayan beef exports, sector leaders believe it could provide a competitive advantage over Brazil, which faces a steep 76% tariff due to political tensions, making Paraguayan beef more attractive in the US market. Paraguay’s exports are expected to double to between 6 thousand mt and 8 thousand mt monthly later this year. However, the country has already exceeded its tariff-free quota and now pays a combined 36% rate. Despite this, beef shipments have surged, with H1-2025 revenues rising 32.44% year-on-year (YoY) to USD 1.24 billion. Meanwhile, Brazil’s agricultural sector is confronting severe losses from the tariffs, with export revenues projected to drop by nearly half, threatening the stability of its agricultural insurance system, already weakened by subsidy cuts.

South Korea

Policy Support and Consumer Trust Drive Optimism for Korea’s Beef Sector

Korean Hanwoo beef remains highly valued by domestic consumers, with supermarkets serving as the primary purchase channel. Notably, November emerges as the peak sales month due to Korean Beef Eating Day promotions. A 2024 consumption trend survey showed that while preference for Hanwoo slightly declined to 74% YoY, it still far surpassed imported beef, being rated superior in taste, safety, and quality, though weaker on price competitiveness. Rising concerns over origin labeling violations have made country of origin the top purchasing criterion, further reinforcing Hanwoo’s premium image. At the policy level, the enactment of the long-awaited Korean Beef Act, defining Hanwoo, ensuring production cost guarantees, and limiting corporate participation, is expected to strengthen sustainability, alongside the recent ban on imports of 30-month-old US beef. However, challenges persist, including high feed costs and competition from duty-free imports, prompting industry leaders to push for lower input costs, carbon-neutral production, and tailored promotions to secure the long-term future of the Korean beef industry.

2. Weekly Pricing

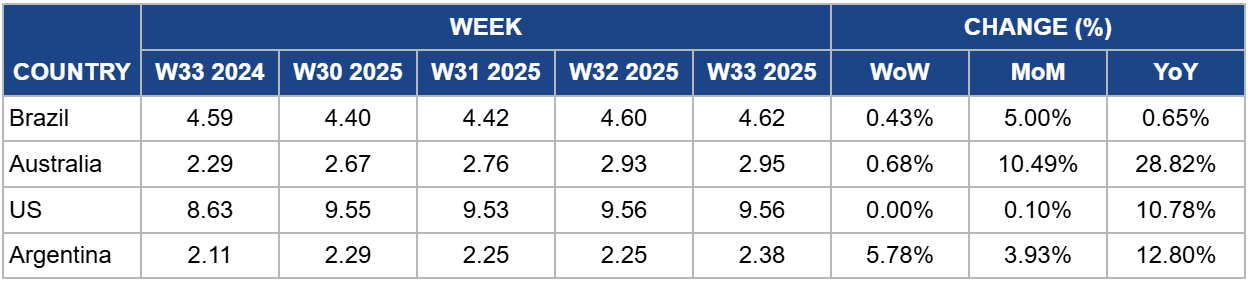

Weekly Beef Pricing Important Exporters (USD/kg)

Yearly Change in Beef Pricing Important Exporters (W33 2024 to W33 2025)

Brazil

In W33, Brazil’s wholesale price for boneless rear beef rose 0.43% week-on-week (WoW) to USD 4.62/kg, reflecting a 5% month-on-month (MoM) and 0.65% YoY increase. Safras & Mercado reported that the wholesale market saw firm wholesale prices during the week due to stable beef demand. However, analysts see limited room for further adjustments in the second half of the month amid weaker seasonal demand. Beef also faces pressure from cheaper proteins like chicken and pork, shaping the short-term outlook. In the physical market, meatpackers secured higher WoW purchases to expand slaughter scales at prevailing prices.

Australia

In W33, Australia’s National Young Cattle Indicator (NYCI) rose to USD 2.95/kg, up 0.68% WoW, 10.49% MoM, and 28.82% YoY. According to Meat and Livestock Australia (MLA), the national cattle market showed slight easing across most indicators, except for the feeder indicators. The feeder heifer indicator recorded the strongest gain, offsetting declines in other categories, driven by robust restocker and feeder demand at Dalby and Forbes, alongside an additional 156 heads in supply. Cattle yardings increased by 1.74 thousand heads overall, though cow numbers declined. Restocker yearling heifer and steer indicators also posted gains, while the processor cow Indicator held relatively stable. Regionally, prices were steady in New South Wales (NSW), firm in Queensland, and eased in Victoria. However, scattered showers in Queensland limited demand for cows, contributing to softer prices. Overall, cow prices moderated compared to last week’s highs, with easing noted across Victoria, Queensland, and NSW.

United States

In W33, US lean beef (92%–94%) averaged USD 9.56/kg, unchanged WoW but up 0.10% MoM and 10.78% YoY. The sustained price rise is largely driven by seasonal peak demand during summer, compounded by tight supplies stemming from lower cattle herds, recent tariff hikes, and border closures with Mexico due to the screw-worm outbreak.

According to the United States Department of Agriculture (USDA), total US cattle inventory stood at 94.2 million heads as of July 1, including 28.7 million beef cattle. This reflects a modest recovery from Jan-25 levels of 86.7 million total cattle and 27.9 million beef cattle, though inventories remain 1% lower YoY compared to Jul-23.

The 50% tariff increase on Brazilian beef, introduced in Aug-25, is expected to reshape trade flows, while continued border disruptions with Mexico may further constrain supply. In this environment, Argentina, Australia, Paraguay, and Uruguay are likely to benefit, as they continue operating under the 10% baseline tariff introduced in Apr-25.

Argentina

In W33, Argentina’s average steer beef price rose 5.78% WoW to USD 2.38/kg, reflecting a 3.93% MoM and 12.80% YoY increase. The price surge was partly driven by heightened demand around the national holiday on August 17, commemorating the death of General José de San Martín. Structural demand growth has also supported prices. According to the Ministry of Agriculture, beef per capita consumption reached 50.24 kg in Jul-25, reflecting a rebound in household demand. This trend is linked to the improvement in real purchasing power, as wages have risen by 52% over the past year, according to the National Institute of Statistics and Census of Argentina (INDEC), covering both public and private sector workers. For Argentines, beef remains a cultural staple. Therefore, for many Argentines, additional income is first directed toward beef before other products, further reinforcing the upward price trend.

3. Actionable Recommendations

Strengthen Domestic Resilience Against Imports

Argentina should prioritize policies that reduce reliance on Brazilian imports by lowering export duties on local beef. This will ensure improvement of domestic beef competitiveness. Incentives for productivity gains, coupled with stricter sanitary controls, would also reinforce confidence in export markets like Chile, mitigating risks from FMD concerns. Furthermore, channeling subsidies toward logistics efficiency and cold-chain infrastructure could help reduce costs across the supply chain, ensuring that domestic production continues to meet rising consumption without being undercut by imports.

Leverage Market Diversification for Strategic Gains

Brazil should capitalize on recent diplomatic and trade missions by fast-tracking sanitary negotiations with premium markets such as Japan. Brazil should also accelerate redirection strategies toward Arab nations to absorb products diverted from the US. At the same time, investments in traceability, animal health certification, and marketing campaigns highlighting sustainability could strengthen Brazil’s global reputation as a reliable supplier. By aligning export diversification with rising demand in Asia and the Middle East, Brazil can reduce its vulnerability to tariff shocks and political disputes.

Maximize Competitive Advantage in the US Market

Paraguay should strategically leverage the tariff disparity with Brazil by negotiating long-term supply contracts with US buyers, emphasizing reliability and competitive pricing despite its moderate tariffs. Expanding processing capacity and upgrading compliance with US sanitary and traceability requirements could boost Paraguay’s export credibility, allowing it to scale shipments sustainably. Policymakers should also explore bilateral agreements with the US to expand tariff-free quotas, which would solidify Paraguay’s emerging position as a more favorable supplier relative to Brazil.

Enhance Hanwoo’s Premium Positioning

To sustain Hanwoo’s dominance, South Korea should strengthen consumer trust through digital origin-tracing systems that address labeling concerns while highlighting superior taste and safety attributes. Policymakers can support producers by expanding subsidies for feed cost reductions and promoting carbon-neutral certification, reinforcing the image of Hanwoo as both premium and sustainable. Targeted marketing campaigns, especially during peak sales months, could further solidify loyalty, while industry partnerships with retailers may help counter the growing price gap with imports.

Sources: Tridge, Agrolink, Bichos de campo, Canal Rural