W32 2024: Maize Weekly Update

1. Weekly News

Europe

Dry Weather in Black Sea Region Prompts Corn Harvest Forecast Adjustments in EU and Ukraine

Dry weather in the Black Sea region has prompted analysts to revise corn production forecasts for the European Union (EU) and Ukraine for the 2024/25 marketing year (MY). The European Commission (EC) lowered its EU forecast by 11% year-on-year (YoY) to 60 million metric tons (mmt), with Romania's estimate reduced by 1.1 mmt to 9.5 mmt and Bulgaria's by 0.4 mmt to 2.6 mmt. Meanwhile, the Ukrainian Grain Association (UGA) cut its forecast for Ukraine's corn harvest by 2.1 mmt to 23.4 mmt. Despite these cuts, corn prices have not risen, as increased feed wheat supply and favorable harvest forecasts in the United States (US) and Brazil have kept prices in check.

Brazil

Brazil's 2023/24 Corn Production Estimate Steady at 116 MMT

In W32, the 2023/24 Brazil corn production estimate remained steady at 116 mmt. Harvest progress for safrinha corn in Mato Grosso reached 99.2%, advancing 2.6% week-on-week (WoW), and is ahead of last year and the five-year average. In Paraná, farmers resumed harvesting after wet weather delays, with 76% of the safrinha corn harvested, showing a 9% weekly increase. However, yields declined for late-harvested corn, with only 42% rated as good. In Mato Grosso do Sul, 49.6% of the safrinha corn has been harvested, significantly ahead of the previous year and average pace.

Brazilian Corn Exports Declined by 16% YoY in Jul-24

Brazilian corn exports fell by 16% YoY in Jul-24, totaling 3.55 mmt, compared to 4,23 mmt in Jul-23. Average daily shipments decreased by 16% YoY to 154,516 metric tons (mt), down from 201,458 mt in Jul-23. This decline is attributed to reduced corn production and increased domestic consumption for feed and ethanol, with projections for this year's total output at 122 mmt and exports at around 40 mmt, down from last year's 137 mmt and record 55 mmt, respectively. Revenue from corn exports also dropped, totaling USD 710.3 million in Jul-24 compared to USD 1.04 billion in Jul-23.

Brazil's August Corn Exports Projected at 6.29 MMT

The National Association of Cereal Exporters (ANEC) estimates that Brazil's corn exports will total 6.29 mmt in Aug-24, marking a significant reduction of nearly 3 mmt compared to the 9.25 mmt exported in Aug-23. This decline reflects Brazil's changing market dynamics and export challenges this year.

Hungary

Hungary Faces Severe Drought and Extreme Heat, Accelerating Crop Ripening and Soil Dryness

Hungary is currently facing a severe drought, with minimal rainfall expected soon. This has resulted in the premature ripening and drying of corn and sunflower crops, with the top half meter of soil across much of the country becoming exceptionally dry.. The heat has accelerated vegetation development by more than two weeks. The situation is expected to worsen, with temperatures predicted to approach 35°C in southern regions in W33.

Ukraine

Record Heatwave in Ukraine Could Slash 2024 Corn Crop by 6 MMT

Ukraine experienced a record heat wave across most regions in Jul-24, which could reduce the country's corn crop by approximately 6 mmt compared to the previous year's level, according to the Ukrainian Agrarian Council (UAC). While the UAC did not provide an exact forecast for the total harvest, their concerns align with the Ukrainian Grain (UGA), which recently projected a 2024 corn harvest of 23.4 mmt, down from 29.6 mmt in 2023. Corn production in many regions could decline around 30% YoY due to the adverse weather conditions. However, the Ukrainian government holds a slightly less pessimistic view, with the acting finance minister suggesting that late crop yields could decrease by up to 15% in most regions.

2. Weekly Pricing

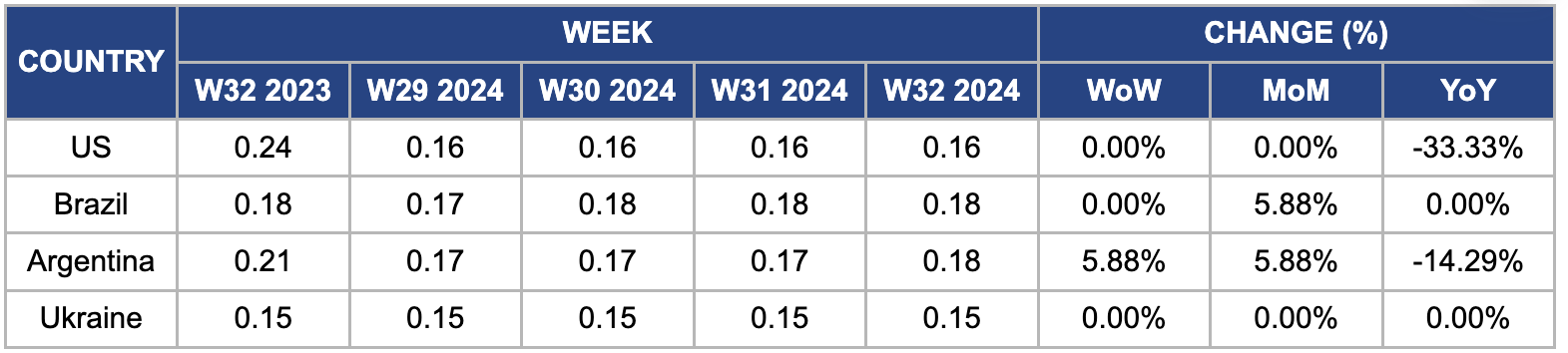

Weekly Maize Pricing Important Exporters (USD/kg)

* Varieties: US (feed grade), all others (overall average)

Yearly Change in Maize Pricing Important Exporters (W32 2023 to W32 2024)

* Varieties: US (feed grade), all others (overall average)

* Blank spaces on the graph signify data unavailability stemming from factors like missing data, supply unavailability, or seasonality

US

In W32, wholesale maize prices in the US remained steady at USD 0.16 per kilogram (kg), but marked a 33% YoY decrease from USD 0.24/kg in W32, 2023. This price drop is due to favorable weather conditions in the corn belt, including cool, rainy weather, improving supply outlooks. Analysts forecast a slight increase in US corn production to 15.112 billion bushels for 2024, despite expected reductions in planted and harvested area due to adverse conditions.

Brazil

Brazilian wholesale maize price remained steady for the third consecutive week, but saw a 5.88% increase month-on-month (MoM). Brazil's corn production forecasts have been lowered, with export projections adjusted downward from the previous season. Demand in Mato Grosso is higher than expected, with a 6.06% increase from the last season, driven by rising corn ethanol plant consumption, which constitutes 73.74% of domestic consumption. Despite this, there's a 9.63% decrease in exports and a 14.26% drop in interstate consumption compared to last season. For the 2023/24 cycle, Mato Grosso is projected to demand 48.15 mmt of corn, slightly more than the previous month but significantly lower than the 2022/23 harvest.

Argentina

The wholesale price of Argentine corn increased to USD 0.18/kg in W32, up 5.88% WoW and MoM. This rise comes amid uncertainty for the upcoming corn season, with a predicted 30 to 60% reduction in planting area due to stagnant input purchases and pest control concerns. Technicians are concerned about pest impacts on early corn planting, with results from monitoring traps pending. Despite recent rains, planting intentions remain down 30% from last year, and input purchases remain stagnant. The pre-campaign outlook depends on improved international prices or better rainfall in Aug-24 and Sept-24. Additionally, there is concern over the evolution of the chicharrita pest following a solid cold period in Jul-24 and Aug-24, with recent data showing an increase in hours with temperatures below zero.

Ukraine

The wholesale price of Ukrainian maize remained unchanged at USD 0.15/kg for the past four weeks. Ukraine experienced a record heat wave in Jul-24, which may reduce the country's corn crop in the upcoming months. The UGA projected a 2024 corn harvest of 23.4 mmt, down from 29.6 mmt in 2023, which could signify a price increase in the upcoming weeks. The heat wave could lead to a 30% YoY decline in corn production across many regions. However, the Ukrainian government is more optimistic, with the acting finance minister suggesting a potential 15% decrease in late crop yields in most areas.

3. Actionable Recommendations

Implement Strategic Harvesting and Storage Solutions

Countries like Ukraine, Hungary, and Brazil should adopt strategic harvesting and storage solutions to counter adverse weather impacts on corn production. Investing in advanced harvesting equipment, such as combining harvesters with moisture sensors, can optimize yield by accurately gauging the best time to harvest. Additionally, enhancing storage facilities with controlled environments to manage moisture levels and implementing pest control measures will reduce post-harvest losses and prevent spoilage. These practices will help stabilize corn supply and quality, ensuring resilience against weather-related challenges and maintaining a consistent market presence.

Enhance Export Market Diversification

As top global corn exporters, Brazil, Ukraine, and Argentina should prioritize diversifying their export markets to better navigate production and pricing fluctuations. Expanding into emerging markets in Southeast Asia, the Middle East, and North Africa can reduce reliance on traditional significant buyers like China and the EU. Establishing trade agreements and fostering strong partnerships in these regions will stabilize their corn revenue and strengthen market presence, providing a buffer against potential production challenges. This strategic approach will ensure sustained growth and resilience in the global corn market.

Optimize Domestic Consumption and Market Dynamics

Brazil, Argentina, and the EU should optimize domestic consumption strategies and market dynamics to address reduced corn production and export challenges. Enhancing the use of corn in local industries, such as ethanol production in Brazil and feed in Argentina, can help absorb domestic supply and stabilize prices. Additionally, improving market infrastructure and supply chain efficiency will support better price management and reduce fluctuations. Implementing data-driven approaches to forecast demand and adjust production plans accordingly will help these regions maintain stability in their corn markets despite external pressures.

Sources: Tridge, UkrAgroConsult, Portal Do Agronegócio, NoticiasAgricolas, Heti Világgazdaság, Hellenic Shipping News, Agromeat