1. Weekly News

Argentina

Argentina's Soybean Planting Progress for 2024/25 Season Reached 54%

As of December 15, soybean planting for Argentina's 2024/25 season has reached 54% of the planned 17.914 million hectares (ha), according to a survey by the Ministry of Economy. This marks progress from 47% in the prior week but slightly lags behind last year's 55% for the 2023/24 crop season, which covered 16.564 million ha. Favorable weather supported crop development between December 8 and 14, including well-distributed rainfall across the core-producing regions and higher precipitation in Southeast Buenos Aires. However, December 15 to 21 forecasts indicate reduced and irregular rainfall, which could challenge moisture availability in key areas.

Brazil

Brazil's 2024/25 Soybean Harvest Progresses Amidst Mixed Weather Conditions

Brazil's 2024/25 soybean harvest is progressing well, supported by recent rains that have boosted crop development across most of the country. With planting nearly complete, attention has shifted to weather conditions, which remain a mix of favorable and challenging. In Paraná, extended rainfall and overcast skies have slightly prolonged crop cycles, though continued precipitation is expected to aid growth. However, the north and northeast regions face moisture deficits in sandier soils, necessitating replanting in some areas. Brazil estimates soybean production at 171.5 million metric tons (mmt) for this cycle, with revisions anticipated in Jan-25 as the harvest begins.

China

Soybean Shortages in Southern China Trigger Supply Disruptions and Price Surge

China's efforts to curb agricultural imports have led to a soybean shortage in southern regions, particularly affecting the oilseed processing hub of Dongguan in Guangdong province. Traders report customs delays exceeding 20 days compared to the usual five, disrupting supply chains. The shortage has forced some soybean crushers to suspend operations for three weeks. This supply disruption has driven soybean meal prices in Guangdong up by nearly 7% week-on-week (WoW) in W50, marking the most significant surge since Mar-24, as demand for animal feed outpaces availability.

India

India’s Soybean Imports Dropped 15% YoY

India's soybean import declined by approximately 15% year-on-year (YoY) in the first two months of the 2024/25 marketing year (MY) as farmers delayed sales, hoping for higher prices. Current market rates of USD 4.95 per metric ton (mt) remain below the Minimum Support Price (MSP) of USD 5.7/mt, adding to the bearish sentiment this season. Analysts project soybean carryover stocks for 2024/25 at 11,160 mt, a significant increase from 24 thousand mt in the previous year.

Paraguay

Paraguay's Soybean Industry Reaffirms Global Standing in 2023/24

Paraguay produced 11 mmt of soybean for the 2023/24 season, with an average yield of 3 mt/ha across 3.65 million ha. This production generated approximately USD 4 billion, reinforcing Paraguay's status as a leading global producer and exporter. By Nov-24, 7.8 mmt had been exported, primarily to Argentina, Brazil, and Russia. Paraguayan soybeans now reach 56 markets and the country is working to secure new opportunities amidst anticipated challenges from stricter European Union (EU) regulations. Although direct exports to the EU are minimal, Paraguay indirectly supplies the market through Argentine soybean oil and meal exports.

2. Weekly Pricing

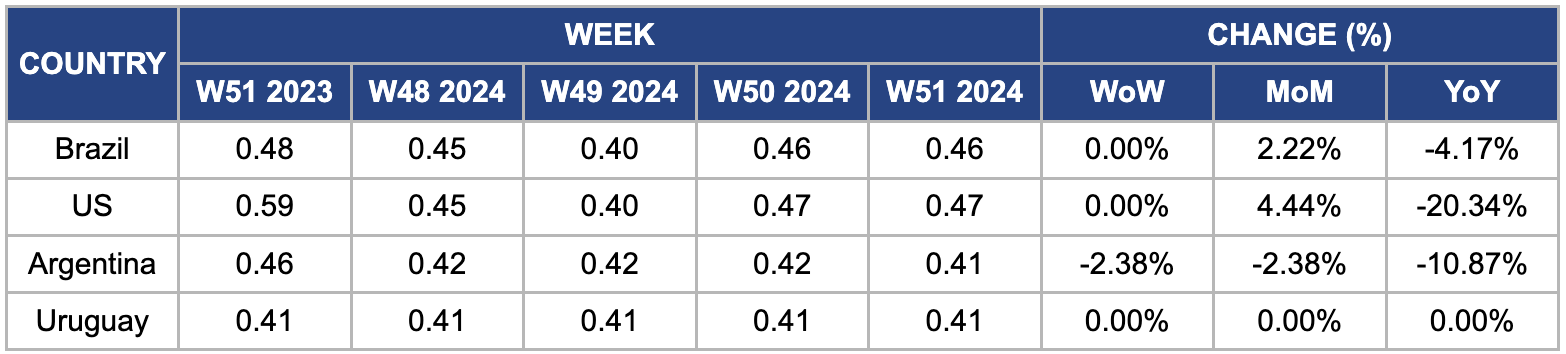

Weekly Soybean Pricing Important Exporters (USD/kg)

Yearly Change in Soybean Pricing Important Exporters (W51 2023 to W51 2024)

Brazil

In W51, Brazilian soybean prices remained stable WoW but increased 2.22% month-on-month (MoM), reaching USD 0.46 per kilogram (kg). This price rise is due to the ongoing soybean shortage, which continued into Dec-24. The delayed planting for the 2024/25 harvest is expected to reduce soybean exports on Jan-25, contributing to a significant drop in Brazilian soybean shipments. In Nov-24, soybean exports fell to 2.55 mmt, marking a 50.87% YoY decrease. From Jan-24 to Nov-24, total soybean exports amounted to 96.81 mmt, a slight 1.26% decrease YoY. Despite these challenges, Brazil's 2024/25 soybean harvest remains promising, bolstered by beneficial rainfall that has supported crop development nationwide. While planting is nearly complete, attention is now on weather patterns, with localized concerns in Paraná, where recent rains have extended the growth cycle for some crops.

United States

In W51, United States (US) soybean prices remained stable WoW but increased by 4.44% MoM, reaching USD 0.47/kg. Several factors drove this price uptick. The National Oilseed Processors Association (NOPA) reported that soybean crushing in Nov-24 was 5.26 mmt, a decrease from the previous month’s 5.44 mmt and below market expectations, indicating a tightening of domestic supply. Moreover, the price surge was fueled by robust export demand, particularly from China. Growing concerns over adverse weather conditions potentially impacting soybean production in South America, further supported the price increase.

Argentina

In W51, Argentinian soybean prices declined by 2.38% WoW and MoM, reaching USD 0.41/kg. This marks a 10.87% YoY decrease from USD 0.46/kg in W51 2023. The price drop was due to a combination of factors, including reduced export demand, an abundant domestic harvest that boosted supply, and the depreciation of the Argentine peso (ARS), which made soybeans more affordable for local buyers. Furthermore, the slow recovery of the Chinese market, a major importer of soybeans, and increased global competition from other key producers like Brazil further pressured prices downward. Moreover, as of December 15, soybean planting for Argentina's 2024/25 season had reached 54% of the planned 17.914 million ha, reflecting progress from the previous week's 47%.

Uruguay

Uruguay's soybean prices remained steady at USD 0.41/kg in W51, supported by several key factors. A strong Uruguayan peso (UYU) helped mitigate the impact of exchange rate fluctuations, contributing to price stability despite global market volatility. Strong international demand, particularly from major buyers like China, played a crucial role in maintaining prices, especially amidst supply concerns from other producing regions. Additionally, carryover inventory from the 2023 harvest acted as a buffer against potential yield declines, ensuring a consistent supply despite unpredictable weather conditions.

3. Actionable Recommendations

Diversify Export Markets for Paraguayan Soybeans

Paraguay has established itself as a major global producer and exporter of soybeans, with the bulk of its exports directed to neighboring Argentina, Brazil, and Russia. However, the increasing regulatory pressures from the EU, which affects exports indirectly through Argentina, create a need for diversification. To mitigate these risks, Paraguay should target emerging markets in Asia, particularly in Southeast Asia (Vietnam, Indonesia) and South Asia (India, Bangladesh), where growing demand for soybeans and derivative products like soybean oil and meal presents a significant opportunity. Moreover, expanding into African markets such as Egypt and Kenya, which are seeing rapid economic growth and an expanding middle class, could provide new demand channels. A concerted effort to establish long-term trade agreements with these markets will help maintain consistent export volumes and reduce Paraguay's dependence on traditional markets.

Invest in Moisture Management and Water Conservation

Brazil's soybean production is robust in regions like Mato Grosso and Paraná. Still, the northern and northeastern states, including Maranhão, Piauí, and Bahia, face significant moisture deficits due to their sandy soils and irregular rainfall patterns. Farmers in these regions should implement advanced moisture management practices to address this. One option is to adopt precision agriculture technologies, such as soil moisture sensors and automated irrigation systems, to monitor and optimize water usage based on real-time data. Furthermore, planting drought-resistant soybean varieties, such as the "Tupi" and "Brasmax" series, developed for Brazil's more challenging growing conditions, can help maintain yield potential despite water scarcity. Another approach is incorporating rainwater harvesting systems, which can capture and store rainfall for irrigation during dry spells.

Expand Soybean Processing Capacity in India

India’s soybean market has grown steadily, driven by rising domestic demand for vegetable oils, animal feed, and other soybean products. However, the country still faces a supply gap due to limited domestic processing capacity, making it reliant on imports. To address this, India should invest in expanding its soybean-crushing infrastructure, particularly in key producing regions like Madhya Pradesh and Maharashtra. Promoting high-oil and high-protein soybean varieties such as "JS 335" and "NRC 37" could improve processing efficiency. Increasing locally processed soybean oil and meal would reduce price volatility and strengthen India’s value-added soybean industry. Additionally, exploring products like soybean-based snacks and plant-based proteins could tap into the growing health-conscious consumer market.

Sources: Tridge, MercoPress, Portal Do Agronegócio, UkrAgroConsult